How Does Financial Stress Affect Your Health?

Financial stress is a global issue affecting millions, including students, families, and professionals. It refers to the anxiety and emotional strain caused by an individual's financial situation, such as difficulties paying bills, managing debt, or meeting everyday expenses, which can lead to worries about money. In this article, we will explore financial stress, its causes, and the significant effects of financial concerns on mental and physical health. We will also tackle the specific impact of financial stress on international students and offer strategies to help them manage stress and this burden effectively.

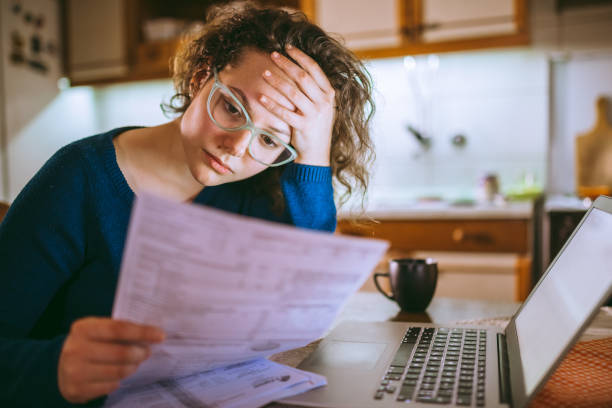

The relationship between financial stress and health is increasingly evident today. From physical ailments to mental health challenges, the effects of both financial worries and stress are deeply felt across all levels of society. A Bankrate Survey in March 2024 revealed that many U.S. adults think their mental health is negatively affected by financial pressures. About 65% blamed broader economic challenges, with 59% citing difficulty covering everyday expenses as a major issue.

In 2024, financial stress has reached alarming levels. Nearly half of Americans, 47%, say this has been the most financially stressful year, according to the survey by the MarketWatch Guides team. 42% admit they avoid checking their bank balance out of fear. For 65% of respondents, money is the most stressful aspect of life, while 88% report experiencing financial stress overall. Younger generations, in particular, feel the weight of these pressures more intensely.

When financial worries become overwhelming, they affect every aspect of a person's life. People suffering from financial stress may constantly worry about their bank balance, ability to pay utility bills, and how to manage medical bills or expenses like car repairs. Financial stress does not just arise from a lack of money. Still, it can also be caused by poor financial planning, mismanagement of credit card debt, or being unprepared for emergencies due to a lack of emergency funds.

Financial stress can arise from various sources, and it's not limited to individuals with limited financial resources. Even stable-income people can face financial worries due to poor financial planning or unexpected financial difficulties. Here’s an in-depth look at some of the most common causes of financial stress:

Debt is one of the most significant causes of financial stress, particularly when people are burdened by high-interest debt such as credit card debt or student loans. In these situations, the pressure of making regular payments, often with mounting interest rates, becomes overwhelming. For instance, if an individual carries a credit card balance for an extended period, they may pay much more than the original purchase amount due to compounding interest. This type of debt can feel like a never-ending cycle that is difficult to escape.

High interest rates can make paying off even small amounts challenging. Over time, the debt grows, making it harder to manage and contributing to constant stress.

Many loan repayments begin shortly after graduation, often before they have found stable employment. The burden of these loans and potential job insecurity can exacerbate feelings of financial strain.

Debt stress often leads to other forms of distress, such as psychological stress and strained relationships. Individuals may feel trapped or powerless, especially when debt payments consume a significant portion of their monthly income. According to a survey by Money and Mental Health, 86% of nearly 5,500 respondents who experienced mental health problems reported that their financial situation had made their mental health worse. This highlights how debt can consume significant monthly income, leaving individuals trapped.

Life is unpredictable, and unplanned or emergency expenses are inevitable. These unexpected costs can severely disrupt even the most well-planned budgets, whether a medical emergency, a sudden car breakdown, or an urgent home repair.

Many people do not have an adequate emergency fund, so they must rely on credit cards or loans or dip into savings for other purposes when unplanned expenses arise. This creates a snowball effect: the more debt someone incurs due to these emergencies, the more financially stressed they become.

For example:

Medical emergencies can result in significant out-of-pocket costs, even for people who have health insurance. Those without insurance or with insufficient coverage are at an even higher risk.

Car repairs are another common unplanned expense that can’t be delayed, especially for individuals who rely on their vehicles for work or daily necessities.

The inability to cover such expenses without going into debt intensifies financial stress, as individuals feel unprepared and anxious about future potential emergencies.

Households with limited income are particularly susceptible to financial stress because they often struggle to meet basic needs such as food, housing, healthcare, and utilities. Low-income families often have little to no buffer for saving or managing unexpected expenses, creating constant financial pressure.

The daily battle to stretch a tight budget leads to difficult decisions, such as paying the rent or the electric bill, buying groceries, or saving for medical expenses. This ongoing juggling act creates psychological distress and emotional strain, as individuals in these households often feel like they are in a state of constant crisis.

Additionally, low-income households are less likely to have access to resources like financial counseling, emergency savings, or affordable credit, which means they may resort to high-interest loans or credit cards to cover shortfalls, further exacerbating their financial problems.

Losing a job or experiencing a significant reduction in income can be a sudden and devastating blow to a person's financial stability. For individuals without adequate savings or alternative sources of income, the loss of employment can trigger immediate financial concerns, such as how to pay the rent or mortgage, cover medical bills, or even buy groceries.

Job loss or income reduction often results in:

There is a fear of losing one's home or being unable to meet other critical obligations, such as healthcare or educational costs.

An increased reliance on credit to meet everyday expenses further increases debt stress.

This situation is especially stressful for individuals who cannot quickly find new employment or face significant barriers to re-entering the workforce, such as age, health issues, or industry decline. Financial insecurity during periods of unemployment or underemployment can lead to higher psychological distress, as individuals worry about how long they can survive without a steady income.

Periods of economic uncertainty, such as recessions, high inflation, or political instability, can cause widespread financial anxiety. During these times, even individuals with good jobs and financial resources may feel insecure about their future.

Examples of economic uncertainty include:

During an economic downturn, people often lose jobs, businesses close, and investments decline in value. The fear of losing one’s livelihood or seeing hard-earned savings evaporate can create intense financial stress.

When the cost of goods and services rises faster than wages, purchasing power erodes, making it harder for individuals to maintain their standard of living. Over time, this increases financial worries as people struggle to afford necessities.

Economic uncertainty creates a pervasive sense of financial instability and can make it difficult for individuals to plan for the future, leading to constant worry and anxiety. Even those with financial stability may question their long-term security, particularly when faced with volatile markets, rising living costs, or shifting government policies.

Poor financial management and spending habits can contribute to financial stress, even for those with relatively high incomes. When individuals consistently live beyond their means or fail to plan for the future, they may quickly find themselves facing financial difficulties.

Examples of poor financial habits include:

Constantly spending more than one earns, especially on discretionary items, can lead to credit card debt and a lack of savings. Over time, this creates a financial hole that can be hard to climb.

Failing to build an emergency fund or save for long-term goals like retirement can leave individuals vulnerable to financial shocks and increased stress.

Without good financial habits, individuals may feel financially insecure despite having a good income, leading to worries about their future.

The connection between financial stress and health is deeply rooted in the mental and physical aspects of a person's well-being. When an individual is financially stressed, the body responds with a physiological stress response—a reaction designed to deal with immediate danger. However, prolonged exposure to stress without relief or support can negatively affect both mental and physical health.

The mental health implications of financial stress are profound. People who face ongoing financial difficulties often suffer from mental health issues such as anxiety, depression, and mood disorders. Financial stress creates a cycle where mental health problems worsen due to the overwhelming weight of financial concerns, and poor mental health then makes it even harder to deal with financial stress.

Financial worries can lead to a range of emotional and psychological issues, including:

The fear of not having enough money to cover everyday expenses or larger financial obligations can create higher psychological distress, leading to feelings of helplessness, sadness, and hopelessness. Those feeling the strain may experience frequent panic attacks or long periods of psychological distress.

When individuals constantly battle financial difficulties, their emotional responses often suffer. Irritability, mood swings, and frustration can lead to strained relationships with loved ones. It’s not uncommon for financial stress to create emotional responses that damage personal and professional relationships.

In severe cases, overwhelming financial worries can lead to thoughts of self-harm or suicide. The weight of financial strain and the belief that there’s no way out can create desperation, especially for those with pre-existing mental health conditions.

Studies have shown that financial stress impacts cognitive abilities, making it harder for individuals to make sound financial decisions. As financial difficulties mount, this can create a vicious cycle where poor decisions exacerbate the financial situation.

Interesting Fact: Research has highlighted a sobering link between financial stress, debt, and suicide risk. Individuals who struggle with financial difficulties, such as mounting debt, are 20 times more likely to attempt suicide compared to those not facing such pressures. This alarming statistic underscores the severe emotional toll that financial strain can have on mental health. The constant burden of unpaid bills, high-interest debt, and the fear of financial instability often lead to feelings of hopelessness, anxiety, and depression.

In addition to affecting mental health, financial stress has a measurable impact on physical health. The physiological stress response that activates during times of stress triggers the release of hormones like cortisol and adrenaline, which, over time, can cause serious health issues such as:

Chronic stress, particularly financial stress, has been linked to heart disease. Elevated levels of stress hormones increase blood pressure, heart rate, and inflammation, all of which contribute to cardiovascular problems.

Stress can lead to unhealthy behaviors such as overeating or a lack of exercise, contributing to weight gain and obesity. For some, financial stress leads to unhealthy eating habits as they resort to cheaper, less nutritious food options due to budget constraints.

Worrying about money can make it difficult to sleep. Insomnia or poor sleep quality is common among individuals who feel financially stressed. Inadequate sleep only worsens mental health problems and increases the risk of other health-related issues.

A typical result of chronic stress is leaving individuals more prone to illnesses and infections. Those facing ongoing financial pressure tend to suffer from colds, the flu, and other health issues more frequently than those in stable financial situations.

Long-term stress can increase the risk of developing chronic health conditions such as diabetes, hypertension, and gastrointestinal issues. The strain of managing debt or worrying about medical bills can create a downward spiral in both physical health and psychological well-being.

Interesting Fact: Too much financial stress doesn’t just affect your mental health; it can take a severe toll on your body, too. When you're stressed, it triggers a range of bodily reactions, such as an increased heart rate, muscle tension, and rapid breathing. This happens because your body releases hormones like cortisol and adrenaline to help you deal with the pressure. While this response is normal in short bursts, if it continues for a long time—often seen with ongoing financial strain—it can lead to real health problems. Over time, you might develop high blood pressure, high cholesterol, muscle pain, and other physical issues caused by the constant stress.

International and domestic college students face significant financial stress, though international students often experience unique challenges. Many rely on family support, scholarships, or part-time jobs to fund their education abroad, but high tuition fees, everyday expenses, and fluctuating exchange rates compound their financial worries. This mirrors the general struggle among college students, with 70% reporting financial stress from the National Student Financial Wellness Study of Ohio State University. It’s not just about affording tuition—nearly 60% worry about paying for school, while half are concerned about monthly expenses like housing and food.

For international students, the pressure can be even greater, as their ability to stay in the country and complete their education often depends on their financial standing. The lack of access to financial support systems like student loans or government aid, along with visa restrictions and work limitations, makes their situation even more challenging. Many feel overwhelmed, balancing academic responsibilities with financial challenges. In fact, 32% of students in the same study stated above admit to neglecting their studies due to the money they owe, and for international students, the added uncertainty of financial independence can make this even more difficult. Financial stress is a major issue that affects student well-being, regardless of nationality.

Coping with financial stress as an international student requires practical strategies to mitigate the financial burden and reduce psychological distress. Here are some effective ways students can manage financial stress while pursuing their studies:

Careful financial planning is one of the most effective ways to deal with financial stress. Students can better understand their financial health and make informed decisions about managing money by creating a budget that accounts for everyday expenses, tuition, and unexpected costs.

Many institutions offer scholarships, grants, and other financial support to international students. By actively seeking financial aid, students can alleviate financial strain and focus more on their studies.

Students allowed to work can take on part-time jobs, which can help ease financial difficulties. Earnings from part-time work can cover monthly bills and help build an emergency fund for unexpected expenses.

International students often face unique financial challenges while studying abroad. Living in a foreign country can introduce financial difficulties, such as managing tuition, housing, and other living expenses, often without the safety net of family nearby. However, by taking proactive steps, students can protect themselves from financial stress and ensure their time abroad is academically and financially successful. Here are some detailed strategies for international students to protect themselves from financial strain:

One of the most effective ways to prevent financial stress is by enhancing one's understanding of personal finance, commonly called financial literacy. For international students, this involves learning the fundamentals of budgeting, saving, debt management, and investing.

Being financially literate means understanding concepts like interest rates, credit scores, loan terms, and the importance of building an emergency fund. When equipped with this knowledge, students can make more informed financial decisions, such as avoiding high-interest credit card debt or creating a budget that reflects their income and expenses. This helps them avoid common pitfalls like overspending or taking out unnecessary loans.

Universities and financial institutions often offer free financial literacy workshops or online resources. International students should take advantage of these opportunities to understand how to manage their finances effectively. This proactive approach helps them avoid financial difficulties that could disrupt their studies.

Medical emergencies are one of the most common causes of financial stress for international students and expats, particularly in countries with high healthcare costs. Even a minor medical issue could result in substantial out-of-pocket expenses without adequate health insurance. This is where health insurance providers like us come into play.

WellAway offers some of the best health insurance for international students tailored specifically to their needs. These plans cover a range of services, including routine doctor visits, hospitalization, and prescription medications. When considering health coverage, it's also important to evaluate the international students or expat health insurance cost. Understanding the price of coverage in relation to the benefits received can help you make informed decisions.

By investing in a reliable health insurance plan, international students can protect themselves from the financial burden associated with medical emergencies, ensuring they can focus on their studies rather than worrying about how to pay medical bills.

One of the most common financial mistakes among international students is failing to manage money effectively. It’s easy to overspend when adjusting to a new country, with unfamiliar costs and temptations to explore. However, keeping track of spending and staying within a budget is essential to prevent financial difficulties.

Managing money starts with creating a realistic budget based on the student’s income, whether from scholarships, part-time work, or family support. Students should track all everyday expenses, from rent and groceries to entertainment and transportation, to see where their money goes.

A good practice is using financial apps or tools that help monitor spending habits and ensure students stay within their budget. These apps can send reminders about upcoming payments, track bills, and even alert users if they are overspending in certain categories.

By diligently managing money, international students can avoid the financial pitfalls of impulsive spending and maintain better control over their finances. This helps prevent financial stress and builds healthier financial habits that can last a lifetime.

Many universities offer financial support services to help international students manage their finances. These services may include financial counseling, assistance with budgeting, and information on available scholarships or grants.

Seeking these resources can be a lifeline for students facing financial strain. University financial advisors are experienced in helping students navigate complex financial issues, such as paying tuition in installments and negotiating student loan terms or the cost of international student health insurance. They can also offer guidance on finding part-time work opportunities or accessing financial aid programs.

Additionally, many universities partner with local banks and financial institutions to advise students on managing debt, setting up bank accounts, and building credit history. By utilizing these resources, international students can gain the financial knowledge and support they need to alleviate their financial worries.

Protecting oneself from financial stress is not just about financial literacy and budgeting—it’s also about managing the emotional and psychological effects of stress. Being far from home, dealing with academic pressures, and adjusting to a new culture can all amplify financial stress for international students. Therefore, it’s essential to adopt healthy strategies for managing stress. Students experiencing homesickness and other effects of stress should prioritize self-care by:

Many universities provide free or low-cost counseling for students, including mental health support for those overwhelmed by financial stress. Professional counselors can help students develop coping strategies to deal with the emotional toll of money worries.

Engaging in activities like mindfulness, yoga, or exercise can help reduce the physiological symptoms of stress, such as anxiety or sleep disturbances. These techniques can improve psychological well-being and help students regain a sense of control over their financial situation.

Building a support network of fellow students can help international students feel less isolated. Sharing experiences and tips on handling financial stress can provide emotional support and practical advice.

Financial stress is a common issue that can have far-reaching consequences for mental and physical health. Financial worries caused by financial difficulties, such as managing debt, medical bills, and unexpected expenses, can make financial stress worse, leading to poor mental health outcomes. For international students, financial stress adds another layer of complexity to their academic and social lives, making it essential for them to learn how to manage financial stress effectively.

One way to address financial stress is by proactively approaching your financial health. Staying informed, building an emergency fund, and seeking professional support when needed are effective strategies to improve overall well-being. If you're an international student seeking financial assistance, Wellaway offers a comprehensive solution. By applying for our international student loan, you can focus on your studies and worry less about your finances. Visit WellAway today and take the first step towards financial relief!